Good Morning Denver!

Let’s dive right into it. The last 7 days’ activity has looked like this.

| New Listing (1026) Less than last week, still too low for buyers. | |

| Coming Soon (193) Up a little, but not holding out much hope for a spring supply. | |

| Back On Market (230) A lot of contracts are not making it to closing! | |

| Price Increase (151) | |

| Price Decrease (668) Wow, Sellers and Listing Brokers are just not getting it! | |

| Pending (1233) This is a nice number! | |

| Withdrawn (104) | |

| Leased (67) | |

| Closed (1257) Sellers and Buyers finding their way to the closing table in spite of 6% +/- rates. | |

| Expired (379) |

Ragtes, Economic Uncertainty, and National/Global Events don’t seem to be causing much anxiety in this market.

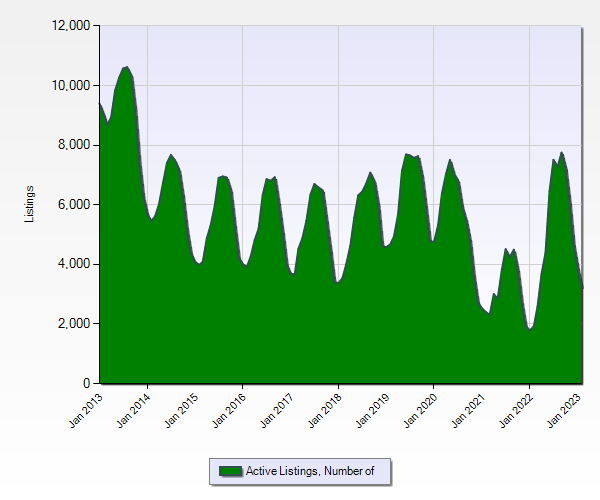

Now, let’s look on the Metro Denver Supply Side.

Inventory has dropped off a rock. We are down almost 600 Active Listings from last week. BUYERS, even with elevated interest rates, are going to find it tough sledding with this supply and demand scenario.

As always, week in and week out, we are fielding questions from our clients, our referrals our friends and our neighbors. What is going on. Residential Real Estate is hyperlocal, even more so than I’ve ever seen. Check in with us for 5 Star advice.

TheCryerTeam@Kentwood.com

Thank You…tc

FYI

Limited Lessening

Monetary policy works most quickly via the most interest rate sensitive sectors of the economy, autos and housing. However, for very different reasons, both sectors have successfully resisted the impact of higher rates. Car sales are rising as semiconductor supply improves, and while housing starts are way down, the number of units, both single-family and multifamily, under construction is staggeringly high, and thus construction employment has yet to decline.

Econ70 – Home of GraphsandLaughs

Elliot F. Eisenberg, Ph.D.

elliot@graphsandlaughs.net

FYI

SUMMARY OF POWELL TESTIMONY (3/7/23):

- Peak rate will be “higher than anticipated”

- Revisions show inflation “higher than expected”

- Minimal deflation in services

- Decisions to be made “by meeting”

- Inflation “to be bumpy”

A pivot from hawkish to more hawkish.

You must be logged in to post a comment.