MyTownCryer Denver Market Watch

THIRD QUARTER 2008

BY TOM CRYER, BROKER ASSOCIATE, THE KENTWOOD COMPANY

303-773-3399 / 800-723-7653

Turmoil in our securities markets, with our financial institutions, and in our own real estate market is always a frightful. As a result, I have taken my semi-annual Denver Market Watch report quarterly to keep everyone up to date. As you read on and examine my charts, you will understand my perspective when I tell you this is just another blip. As the World Turns; so will Denver’s residential real estate market.

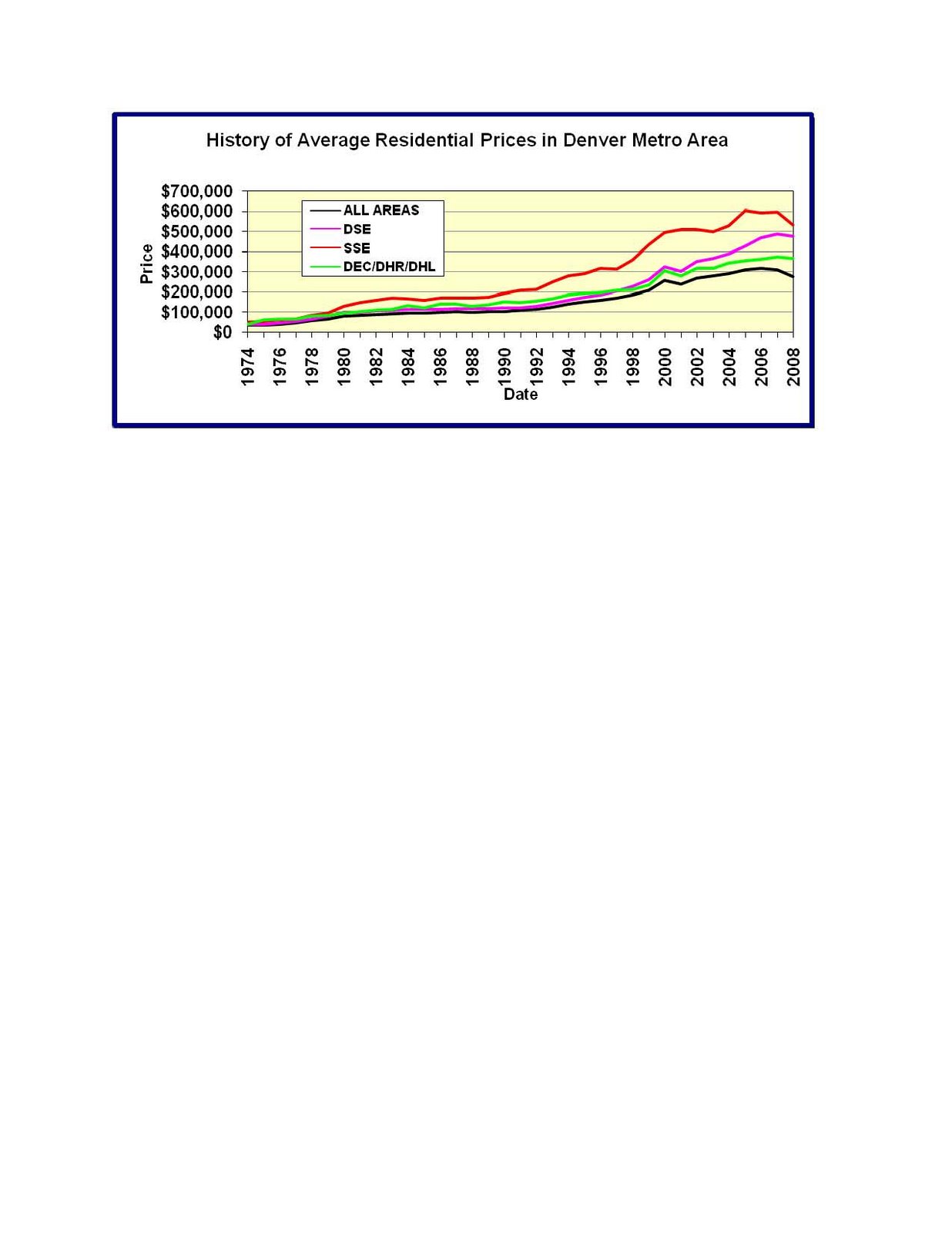

As an example, The History of Average Prices below shows quite a drop in average price for SSE. Don’t worry, this has happened before. If you were to look at The Market Share by Price Range, further down the page, you will see that between $750K and $1M and $1M up, we have had a substantial drop in the percentage of sales activity. The SSE MLS area enjoys the greatest number of +$750K transactions. As a result, when this market segment has a reduction in closings, the average price for the entire MLS area falls.

I like to direct my customers and clients to the notion of affordability. When we are perceived as an affordable market, we attract new business and the employees that follow. With 84% of our MLS transaction activity occurring at or below $400K, we have to be considered an affordable market. On the other hand, with only slightly more than 4 months supply in this market segment as noted below, we are on the precipice of change. Historically, should this fall below 4 months supply, we will start to see a dramatic change. This ratio was over 6 months in June of this year. It doesn’t take long for inventory to disappear at ratios below 4 months. If everything were to work in harmony (rates, available credit, fuel costs, etc), we could have an early change in this market segment well before my 2010 pontification. Keep your eyes peeled.

We read much about our foreclosure problems throughout the Metro area, and no county is left unscathed. A myriad of reasons exist for the extraordinarily high numbers, but my estimates for 2008 are based on 3rd Quarter results annualized toward the end of the year. This is basically 600+ foreclosures per week in the metro area. This unequivocally alters the landscape. Not only with yard signs, but family displacement, investment dollars lost, and neighborhood reputations diminished. A similar cycle occurred in the Denver Metro Area during the mid to late 1980s. Remember the RTC days? Denver recovered from that negative cycle, and we had 10 uninterrupted years of relative residential real estate prosperity. I’m predicting another rebound, and I’m suggesting that it could come as soon as 2010.

I can report on the history of sales in our MLS system over the last 30 years, because I’ve been there, and I have the evidence to show below; it’s happened before and it will happen again. During 1977-1978, 1991-1993, and during 1999 into 2000 we had rapidly appreciating markets with multiple offers on listings. Each one of these periods of high demand was subsequently followed by periods of weak demand. During the late 1980s and mid 2000s we have had severe negative influences on our market from foreclosure inventory. If history repeats itself, and it always does, this should put us somewhere in the next 12 to 24 months for a significant rebound. How’s that for a crystal ball?

Data obtained from Metrolist, Inc., Rocky Mountain News, & Denver Board of Realtors.

Compiled by Tom Cryer, SCRP Broker Associate with The Kentwood Company.

{kind=link}